The last article we wrote was here in December. We squeezed it in just before the Bank of England base rate announcement on the 18th December where the base rate dropped by 0.25%.

At the end of that post we said:

- It is looking extremely likely the base rate will drop by 0.25% – which it did.

- Interest rates could be 1% lower than they were this time last year…

So lets take a look at the numbers and see where we are at and if the second “prediction” will come true.

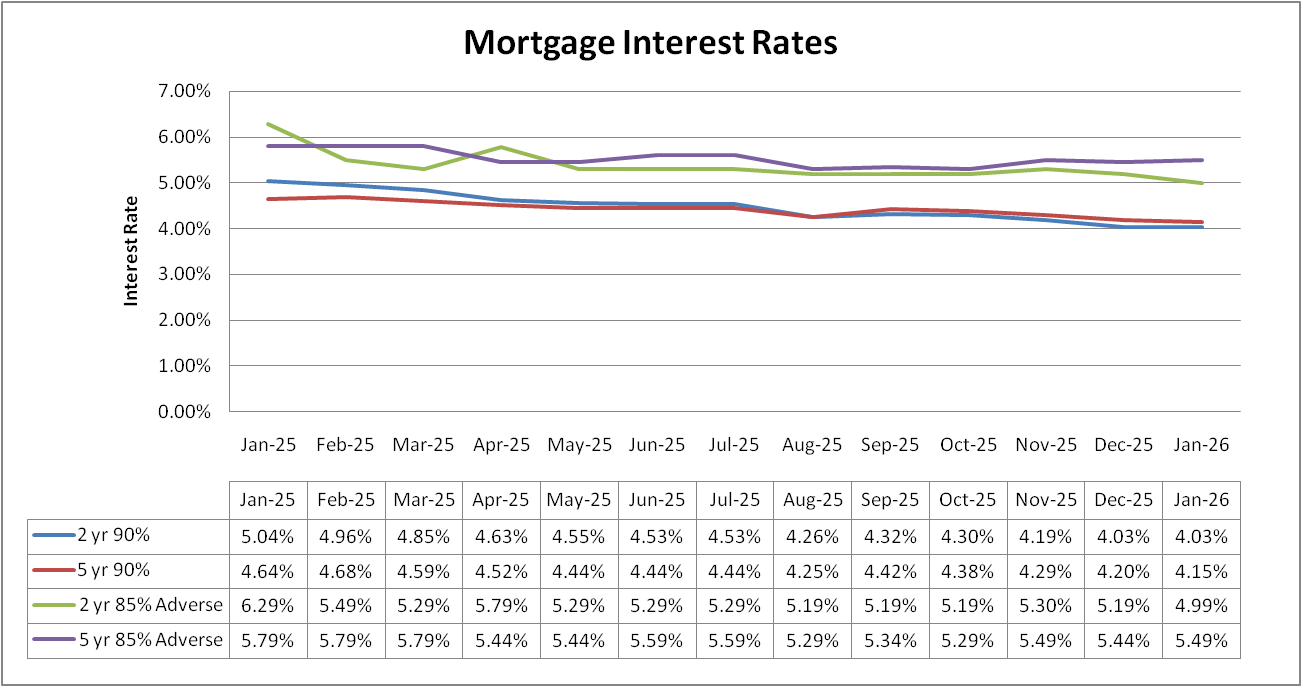

What mortgage rates we are looking at?

As ever, we always look at the same 4 scenarios for some consistency. The 4 scenarios are:

- 2 year fix at 90% LTV with a £999(ish) fee.

- 5 year fix at 90% LTV with a £999(ish) fee.

- 2 year fix at 85% LTV with a £999(ish) fee for adverse*

- 5 year fix at 85% LTV with a £999(ish) fee for adverse*

*Adverse in these examples is someone with 5 defaults from 2 years ago. Enough to mean we cant go to the high street.

What mortgage rates are available now?

Having run the numbers its a a case of mixed results.

- The 2 year fixed rates are both 1% (or more) lower than they were 12 months ago.

- The 5 year fixed rates are closer to half a percent lower than they were 12 months ago.

Why the difference? & Why have they not all come down by 0.25%?

Both good questions!

Mortgage rates are not normally linked to the bank of england base rate. At best they tend to move broadly in line with it.

You might notice that the interest rates dropped between November and December. This was in part because everyone was expecting the base rate to drop – so lenders did some of their rate reductions earlier. But the full 0.25% reduction has not been passed on – this suggests that lenders may still have some space to go in reducing their rates or that they are trying to increase their profit margins – I suspect it will be a combination of the 2 and rates will be a little lower next month than they are today.

In addition to that you can see there is a clear difference between the 2 year fixed rates and the 5 year fixed rates. There is more risk in a 5 year fix, if rates do jump up then you as the customer are protected from that for a period. The bank may not be to the same extent. So that could be why we are seeing the rates dropping much more slowly on the 5 year fixed rates.

Mortgage rates in 2026

In December, we said that the central banks seem keen on getting interest rates down. This is still the case and so it seems likely that rates will continue to come down throughout the year.

Although with the way the world is at the moment, it is possible that could change.

Summary

We are starting the year off in a nice way I suppose. Interest rates are as low as they have been in maybe 3 years. There are signs they will continue to come down.

No matter what you read in the press, if you would like something that is not sensationalised and is unbiased, come and check out our table. We cant do all of the LTVs im afraid, but it gives you a good idea of where the market is for the masses rather than just those with at the lowest LTVs.

If you would like to discuss your options, you know where we are. Please do get in touch.