Bad credit comes in many different forms. In this article we are going to look at the different types of bad credit. We will also look at some statistics regarding bad credit as I think this is important for people who maybe think they are alone. And we will also look into some Success stories we have.

Combined this should help you to see if you can get a mortgage with your bad credit or not.

The different types of bad credit

- Defaults

- CCJs

- Missed/Late payments

- Debt Management Plans (DMPs)

- Insolvency (which includes Bankruptcy, IVAs and DROs).

Most people will have a combination of these. Its almost impossible to have Defaults or a DMP for example without arrears.

Dont worry if that is the case. We have examples of that and how we can overcome it below.

Bad credit causing scenarios

Scenarios are the things that caused the bad credit. Over the years we have seen a lot of reasons for adverse, from some of the worst things imaginable (losing a child for example) through to things like being young and silly.

In order to overcome your adverse its not a case of coming up with a dramatic story, it is a case of understanding what caused it. No matter what the reason, it normally falls into one of the following scenarions:

Ill health is a big cause of adverse

I probably do not need to write war and peace here. We have had tradesmen with broken legs unable to work through to people fighting cancer.

A lifetime event is a catch all for most adverse

Divorce, job loss, we once had a couple who had an unplanned baby…twice! Which really stretched the household finances.

Youth

Many young people are offered credit, overdrafts, store credit etc. There is nothing wrong with that. But taking too much too quickly and being unable to pay it back can become a problem. A personal favourite as it normally means you at least had the good times before the bad!

When we look through credit reports, we can see a 6 year history. The one that tends to cause a problem is if there are defaults spread out over 5-6 of those years. Most credit reports tell a story, so if you have Green markers for 4 of those years and red for 2, then it says there was an issue during that time.

If we see red marks over 5 years then it suggests it was either long standing problem or the problem has not really gone yet. This is the type of adverse that can be difficult to overcome.

Statistics

I think this is a really important section of this post.

It is not uncommon to speak to people who are upset or embarrassed about their adverse and anxious about being able to overcome it. This part is aimed at helping you to see you are not alone and although people do not actively talk about bad credit, there is a large part of the population that have some negative markers on their credit report.

Bad credit can affect anyone, we have customers on minimum wage with benefits and we have customers on 6 figure incomes. Life has a habit of throwing problems and they can catch anyone out.

According to Pepper Money who carried out a survey last year:

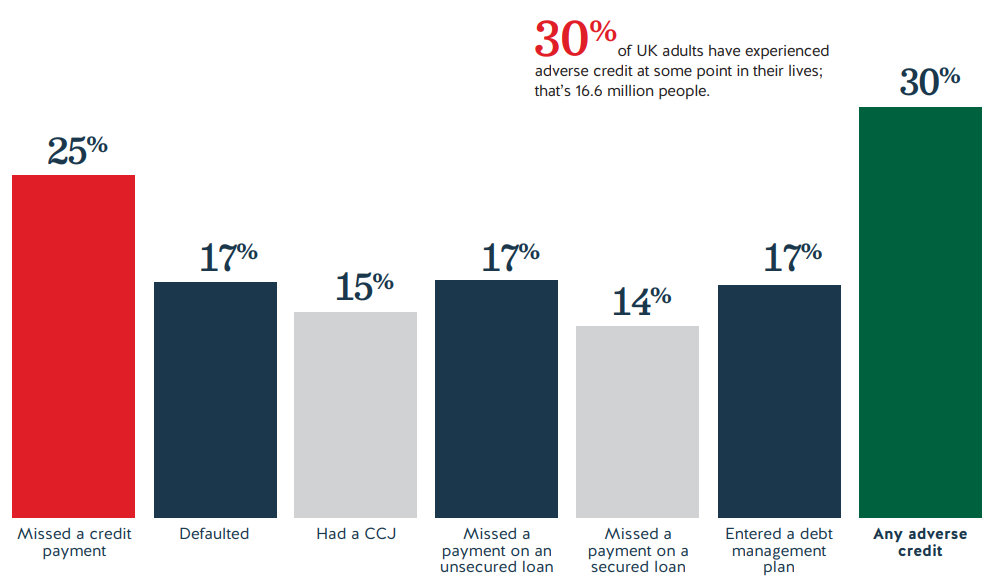

30% of adults (16.6 million!) have experienced adverse credit in their life. You are not alone.

Over 9 million people have experienced bad credit in the last 3 years.

Education does not really play a part

Going back to what I mentioned earlier about income and us seeing customers from all walks of life. Part of the research found that people with no qualifications (ie no GCSEs or above), around 12% had at least 1 CCJ in their life time.

People with a Doctorate (very highly qualified in their field), had a 19% chance of having a CCJ.

The rest of the pack (GCSEs, A levels and Degrees) were around the 15% mark give or take.

Adverse types and their numbers

Lets break down the adverse by type as I think showing everything individually is also important.

17% of the population have had at least 1 default. We are currently working on an application where the applicant has 16 defaults.

15% of the population have had a CCJ. Admittedly, we see less of these. I was not expecting these numbers to be so close when looking through the report. But we do see plenty of them.

17% have entered a DMP. That means almost 1 in 6 people you speak to, are potentially in a Debt management plan.

Insolvency by numbers

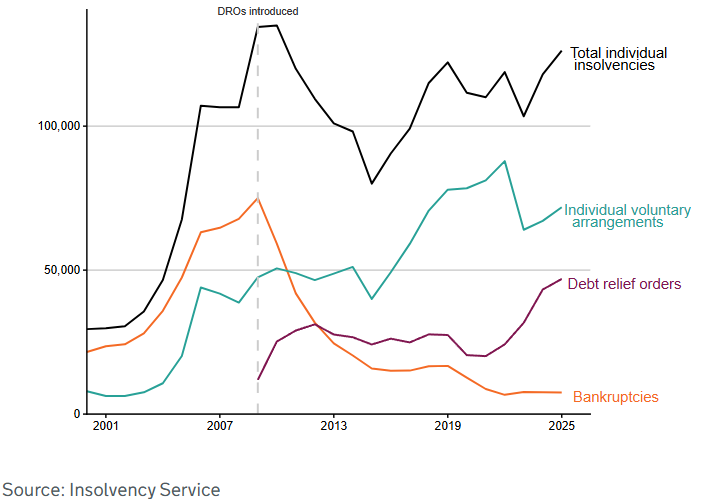

Insolvency covers things like IVAs, Bankruptcy and DROs. According to Gov.uk around 120,000 people per year have gone insolvent in 2024 and 2025.

- The majority of those (57%) were IVAs, 71,841 in 2025.

- This was followed by DROs which accounted for 37% or 46,939.

- Lastly we had Bankruptcies at 6% of 7,460.

Adverse Success Stories

We need to start turning this negativity around though. You know you have adverse, so lets try to find some examples of people who have been in your situation or worse and have been able to get a mortgage…

9 Defaults, Pay day loans and a 10% deposit – not the easiest combination to overcome. A Defaults and Pay day loans success story – This is an example of where we tried to set the clients expectations but we were able to better it.

An IVA that had been settled for 2 years success story. This was a relatively easy case to research. The lender made it far harder than it needed to be. But we did get there in the end.

2 lots of adverse Success Story. I thought this would be a good one as I mentioned earlier about looking at credit reports for a sign of a blip. This one looked more like a habit, but again with “the story” and some additional context, it can make a big difference to the options.

Summary

If you have bad credit, I think it is really important to understand that you are not alone. You are not the first person to have bad credit, you certainly will not be the last.

I really like the saying “There is no point in crying over spilt milk.”. You have bad credit, you can sit and dwell over it or you can get in touch and we can look to find you a solution.

If you do nothing, you wont get a mortgage. If you get in touch, you might…

We can normally tell within a 10 minute conversation whether we can help and give you an idea of rates, fees, deposit amounts etc. There are times, like in the example above we may not get it spot on. But we will always do our best to give you an idea of what is possible or if we think we will struggle we tell you that also.

The worst thing to do is nothing. At least if you know the options you can decide whether you want to proceed or not.