I have held off doing an update for a little longer than usual. Rates have been fluctuating far too much. By the time I did the research and published it, we had emails regarding rate changes.

I always try to ensure what we post is accurate and that was why I started these posts originally. There was so much in the news that was just not accurate or certainly not for the average person. When you read in the posts about rates under 4% you think great… Then when you find out it comes with a huge fee and needs a 40% deposit, the reality is it is not suitable for most people.

Anyway, things seemed to have settled down a little now and so we are due an update.

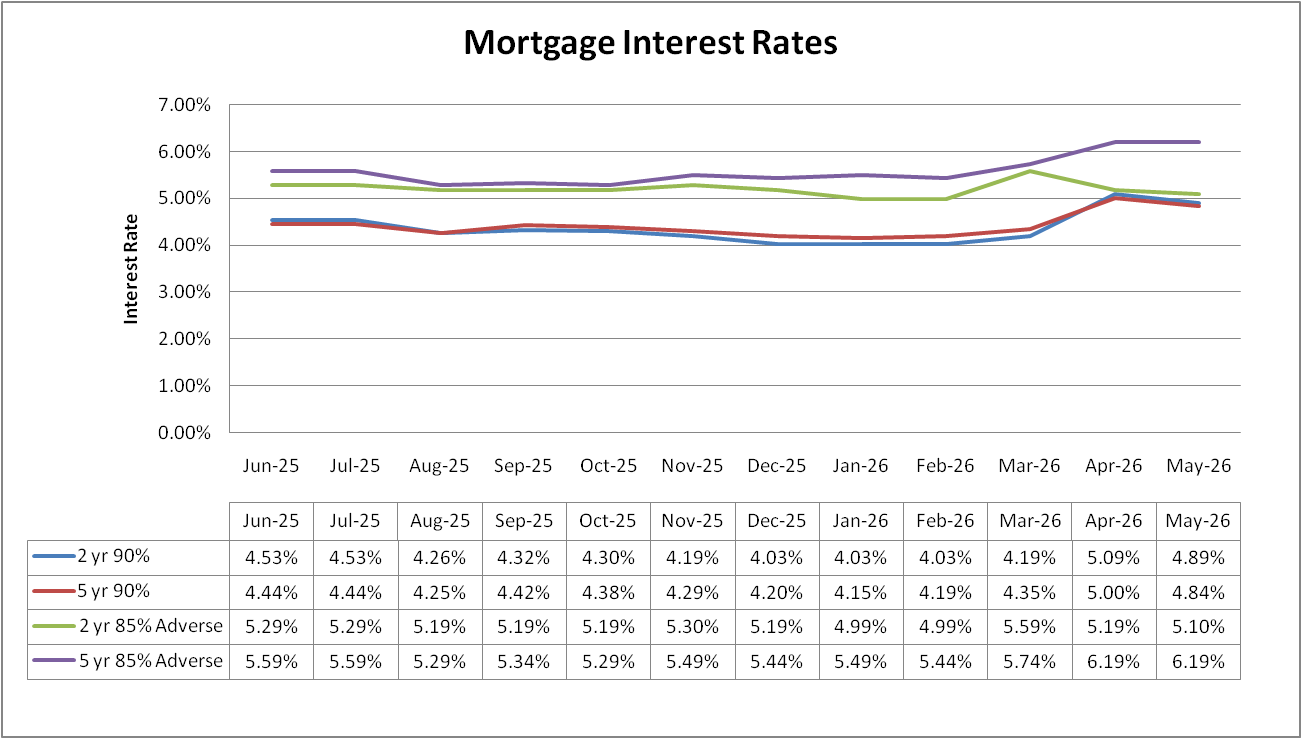

What mortgage rates we are looking at?

As ever, we always look at the same 4 scenarios for some consistency. The 4 scenarios are:

- 2 year deal at 90% LTV with a £999(ish) fee.

- 5 year deal at 90% LTV with a £999(ish) fee.

- 2 year deal at 85% LTV with a £999(ish) fee for adverse*

- 5 year deal at 85% LTV with a £999(ish) fee for adverse*

*Adverse in these examples is someone with 5 defaults from 2 years ago. Enough to mean we cant go to the high street.

With the adverse products, we were able to source 1,292 products.

At 90% LTV we were able to source 1,003 products.

Some of these lenders would not have actually accepted the adverse, some only lend in certain areas and some have large fees. When we put the rates below, we go with the ones we know are likely to accept the majority of people. That means there may actually be lower rates available on the market.

This article is aimed at the average person so it seems fairer to go with a lender who is more likely to accept the average person.

What mortgage rates are available now?

The 2 year adverse product is now only 0.1% above pre US/Iran war levers and below where it was in December! I think that is quite interesting. I have absolutely no idea what to take from it, hopefully it is a sign of where the market will go rather than an quirk.

Everything else is still around 0.5% above pre war levels. However, they have come down by around 0.15% in the last month or so. Again, hopefully a sign of things to come. The war has not spread and so I think that fear which bumped rates up so much has started to subside.

Mortgage rates in 2026

What do we think? I am starting to become reasonably positive. The Bank of England seem reluctant or unlikely to put the base rate up. They have acknowledged inflation will inevitably go up, but it is down to the war in Iran rather than anything else.

I think this, combined with the announcement from Trump and Iran yesterday about a deal being nearly in place, we have likely seen the peak and things should only get better. Time will tell of course.

Summary

I think you just need to live in the moment, decide what is best for you now. That might be taking out an insurance policy mortgage sooner to protect you against rate rises, it might be holding off moving home etc. I dont think anyone can blame you for any decisions you make at the moment with so much unknown.

We do seem to be doing a lot of variable rate products with no ERCs though. One of the benefits of having a broker and talking through the options, most people instantly dismiss these but as soon as you talk about them people become open to them.

Whether you want to proceed, see what is going on or are unsure – feel free to get in touch. Lets have a chat and discuss your options.