This was an unusual enquiry, even for us!

I often say to people that most things can be overcome. The problems tend to start when you have multiple issues. I think the best way to describe it is a Venn diagram.

If we say we start with a pool of maybe 85 lenders.

- Issue 1 might kick out 20,

- Issue 2 another 20 and

- Issue 3 another 20.

All of a sudden you are down to 25 lenders – which is still great, but then what if some of those remaining 25 wont do 2 or 3 of those issues on the same application?

This was the case on this application.

We had a client who wanted:

- Part interest only/Part repayment. This was quite a quirky bit as the stance of lenders varied massively. Some wanted the applicant to have a certain amount of equity at application, others wanted it on completion. Some would not accept the repayment vehicle for the interest only element.

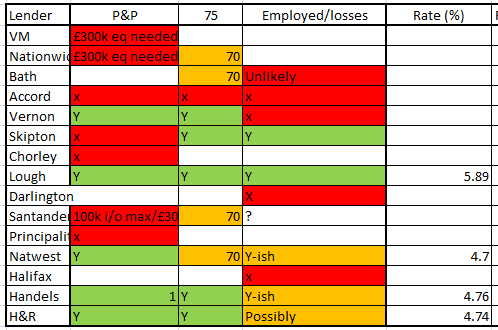

- The mortgage to go to age 75. Generally speaking this was probably the easiest part to overcome. There are plenty of lenders who will go to age 75 but as you can see from the table below, it was not for all lenders.

- Their business had lost money (on paper but not in practice). This was a problem. Even some of the lenders who said it was within criteria were not actually ok with it in practice.

The research stage

You can see from the list of lenders below that each issue had lenders who were not open to it with the exception of one.

This list is a reduced list of the research we did. I just wanted to provide a brief overview of what we come across on applications with multiple issues. Even a yes in criteria is not a yes at underwriting. We ran this by a lender who on paper were ok with everything. Because I wanted to be completed upfront and not waste time applying I asked a lender to run it all by the underwriter beforehand to see if they were ok with everything combined…

They came back and said no.

Now that is fine, it was partly expected (hence why I wanted it run by them in advance). It helped to prevent wasting time with a full application and also a credit check.

In the end when we sat down to discuss the options with the client (or lack of) we came to the conclusion that going to age 70 would be a better option than going to 75 but paying an extra 1%. The repayments were slightly higher, but ultimately the balance was coming down quicker and although it might be a stretch for a year or 2, it would start to get easier once a pay rise or 2 has kicked in.

The outcome

In the end we applied to Natwest. Which is interesting as the third column was not a definite yes, so there was a risk involved. However I checked upfront and was being given all the right signs that it would be accepted at full application.

We went ahead as we still have the higher interest rate as a back up option if needed. Within a few days they came back with a couple of questions but all the signs were positive. We supplied the answers and within a few days we had the offer in hand!

This was a great outcome as despite all of the problems and complexities on this application, we were able to secure the client a high street mortgage at normal rates.