This is the second update since the war in Iran started. I have been having so many conversations about how the price of oil can affect mortgage rates! (I still have no idea).

It has all been bad news… until 2 weeks ago and then we seen something we had not seen for a month – a mortgage lender reducing rates!

Time for this months update and I thought showing you some emails we have received recently would give you an idea of what we receive. (Some news ahead of the public announcement below) You can see there will be a lender reducing some rates and increasing others. Another lender has recently reduced selected rates. But I think the key bit is the word in the middle – volatility.

I believe the rate rises has more or less peaked now and so this is the worst it should be more or less. But I suppose a lot depends on whether this war ends or gets worse, I like to think positively.

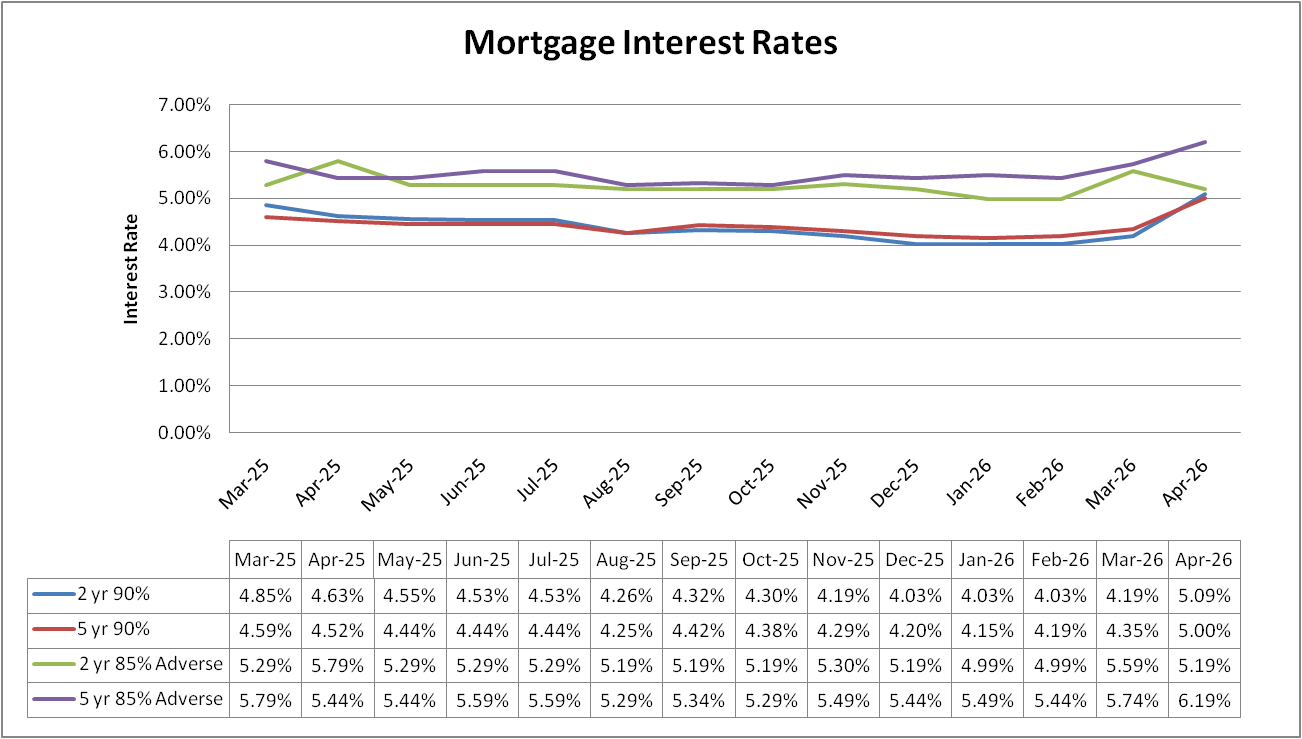

What mortgage rates we are looking at?

As ever, we always look at the same 4 scenarios for some consistency. The 4 scenarios are:

- 2 year deal at 90% LTV with a £999(ish) fee.

- 5 year deal at 90% LTV with a £999(ish) fee.

- 2 year deal at 85% LTV with a £999(ish) fee for adverse*

- 5 year deal at 85% LTV with a £999(ish) fee for adverse*

*Adverse in these examples is someone with 5 defaults from 2 years ago. Enough to mean we cant go to the high street.

What mortgage rates are available now?

Last month my comments at this section were about it all being bad news but the reality was rates had stayed fairly stable.

I think this month is the opposite. With the exception of the adverse 2 year product (which I will explain shortly) there is a very clear jump in rates, give or take we are looking at around 0.5% increases.

The exception is the 2 year adverse, that is down in part to products being pulled last month due to the uncertainty that have been relaunched. Oddly it is the only one of the 4 that is within touching distance of where we were before the war started.

Mortgage rates in 2026

I think we are past the point of guessing at the moment. It all very much hinges on this war. If it stops soon, the expectation is rates will go back down. If it carries on, I dont think that is likely. But my mortgage exams do not make me an economist and I can only pass on what I hear from the “experts”.

Summary

I think you just need to live in the moment, decide what is best for you now. That might be taking out an insurance policy mortgage sooner to protect you against rate rises, it might be holding off moving home etc. I dont think anyone can blame you for any decisions you make at the moment with so much unknown.

We do seem to be doing a lot of variable rate products with no ERCs though. One of the benefits of having a broker and talking through the options, most people instantly dismiss these but as soon as you talk about them people become open to them.

Whether you want to proceed, see what is going on or are unsure – feel free to get in touch. Lets have a chat and discuss your options.