Every now and again we receive a call… “I have found a rate of 4.01%, can you beat it?” or “What is the best rate you can get?”

I try not to get frustrated at these calls as its not uncommon for people to think we are a price comparison service. But if thats what you want, you dont need a broker. You certainly dont need a broker that charges a fee (like us).

We need to get some information

We can give you the lowest rate, it would take 2 minutes. But it does not mean it would be any use for you.

- What is the LTV? (this is the mortgage amount divided by the purchase price). – There is no point me giving you the 60% LTV rate when you have a 10% deposit.

- How much is the mortgage? If you want a £50k mortgage, chances are you would be better off paying a higher rate with no fees. The opposite would be true on a £500k mortgage. Somewhere in the middle there will be a cross over.

- How long do you want to tie in for? 2 years would normally be cheaper than a 5 year deal, but not always.

- A fixed rate or variable?

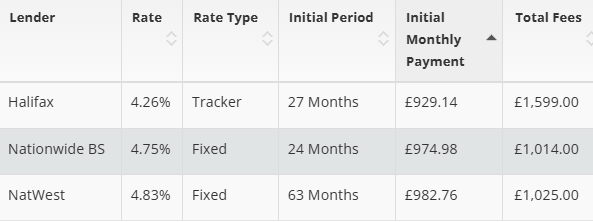

Here is a table below. The cheapest 85% product is 4.26% – but it is a tracker. Most people do not want a tracker at the moment due to world events.

You can quickly see that with a few questions and a bit of discussion, your preference might actually be a product that is over 0.5% higher because it gives you more security. But it might not be.

Research

After a quick chat we have established the type of mortgage you want.

This is where the research kicks in. I did a post on this previously. You can read about what goes into research here.

Ultimately it is still not a case of looking for the cheapest. We still have to check:

- You fit criteria – Employment, credit history, address history etc.

- You fit affordability.

- The property fits criteria – near commercial property, large amount of land, if leasehold does that fit within criteria etc or even something quirky like water coming from a borehole!

You might think you are straight forward, most people do. And most people are right. But every now and again people get it wrong.

Summary

We started with your question of the cheapest rate.

We turned that question around and fired a few back at you. With the answers to those questions we have been able to establish a little more about what you want. It might still be the cheapest mortgage, but it probably wont be.

At some point we would need a factfind for you. This is where we get everything down on paper. With this we go a little deeper and use it for the research.

- Understanding what you want from your mortgage.

- Ensuring you fit criteria and affordability.

- The property is within criteria and likely to pass a valuation.

Once we have done that, we will put your application in. We will deal with enquiries from underwriters and chasing from the agents.

If there are problems with the application we will deal with them.

Once we have jumped through the hurdles and got you your offer, the solicitors will take over. But even then, hopefully by this stage we have built up a rapport and you trust us. You might feel more comfortable picking our brains over the solicitors. Where we can help, we always will.

Conclusion

Do you still want the cheapest rate?

Or do you want a broker that will spend a bit of time with you to make sure you understand the options and ensure that your mortgage is most suitable for you?

Just to be clear, we receive commission from the lenders. But that is not linked to the rate you pay. If you want the cheapest rate, thats perfectly fine. We just want to ensure you know the options before proceeding.