We are half way through the year. I thought now would be a good time to take a look at what sort of things we are doing, trends in the mortgage market and so on. The last couple of months and years have been unpredictable at best. Before the war in Iran started we were seeing 5 months of stability and it was nice to see everything settling down.

Then the war came and the unpredictability came, mortgage rates up, oil prices up, demand down and then everything started to settle down a little. Lets take a look at where we are and what we are seeing…

Mortgage Rates Fixed v Variable

For the first time since we started back in 2013 we are doing almost as many variable rates as we are fixed rates. Historically, I would say about 95% of what we have done is fixed, we are now much closer to 50/50.

On the face of it that might seem crazy but let me explain…

Although mortgage rates generally went up for new mortgages earlier in the year, the base rate has not changed. This means if you are on a variable rate (linked to the bank of england base rate) your mortgage would not have changed.

In addition to that, the governer of the bank of england has recently said that although they expect inflation to go up on the back of the Iran war, that alone is unlikely to be enough for the base rate to go up – you can see more here.

With variable rates being up to 0.8% cheaper in some cases than a fixed rate, it would mean that the base rate would need to go up at least 3 times (assuming 0.25% increases) before the repayments were even close.

When we have this conversation with customers, many are opting for variable rates and I think for a lot of people this is the right decision – time will tell of course. But this is great for mortgage advice as it really shows where we can add value by talking about things you might otherwise dismiss.

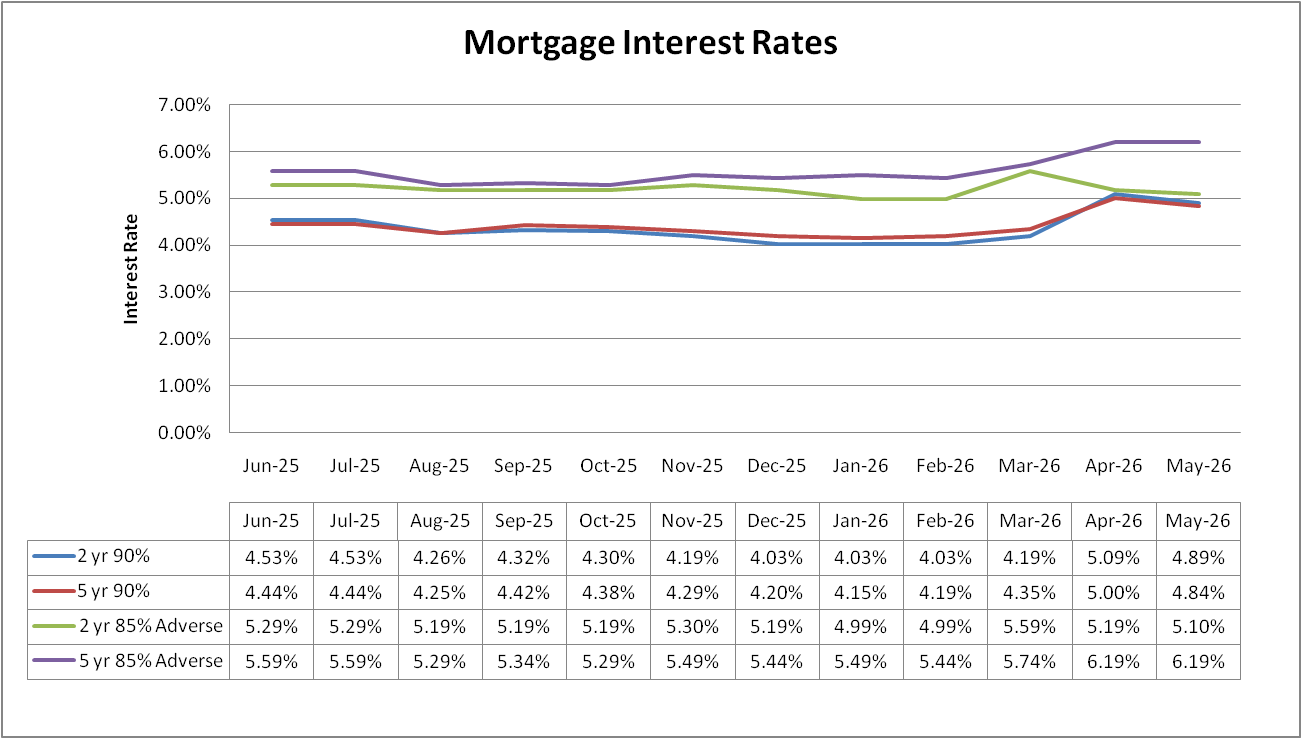

Mortgage rates in general

Every month or so we do a comparison of 4 mortgage scenarios. You can see the latest here but this is the table.

You can see there was a spike in March after America started the war with Iran. Prior to that they were edging down but only marginally. We seem to be back on course for that happening again, especially with the end of the war in sight.

Rates are currently where they were around 18 months ago.

How is business/the market?

It has been a mixed year. We started the 3 months being very busy. But again, once the war started, things started to quieten down and it has generally been on the slower end of what we would normally see ever since.

We can already see house prices are coming down this year. Because of a lot of uncertainty, the pressures on inflation etc these are all putting pressure on house prices as people just cant afford what they once could. Add in the fact that it is a World Cup year (we tend to see it go quiet during the WC and the Euros), that might also put pressure on house prices. Less buyers and people who want to move are maybe prepared to accept those cheeky offers.

After being very much ahead of where we expected to be to probably slightly behind it shows that Q2 (April-June) have not been the busiest. On the upside, we are finally caught up on admin, enjoying the sunshine and of course the football – every cloud and all that!

Summary

If you are looking to buy, I think its a buyers market. The second half f the year I think is going to be slow for brokers, house sellers and estate agents – it might be a good time to drive a deal with the agent, not your broker though, they need looking after 🙂

I think rates will continue to come down – famous last words – albeit slowly.

Assuming Andy Burnham becomes the next PM, the markets seem to be quite comfortable with that and everything is relatively stable. So fingers crossed for a nice steady second half of the year.