Since the last update there has been a Bank of England base rate update – which was to hold things as they are.

That was completely expected, there were no real changes in mortgage rates in the weeks leading up to it, which is what we would expect to see if there was going to be a change.

Things are still relatively calm. We have had a few emails this week from a couple of lenders lowering rates. They seem to be relatively minor rates so before I do the research, I am expecting to see some slight decreases in the non adverse products. The adverse products I think will be very similar, if not the same as they were last month.

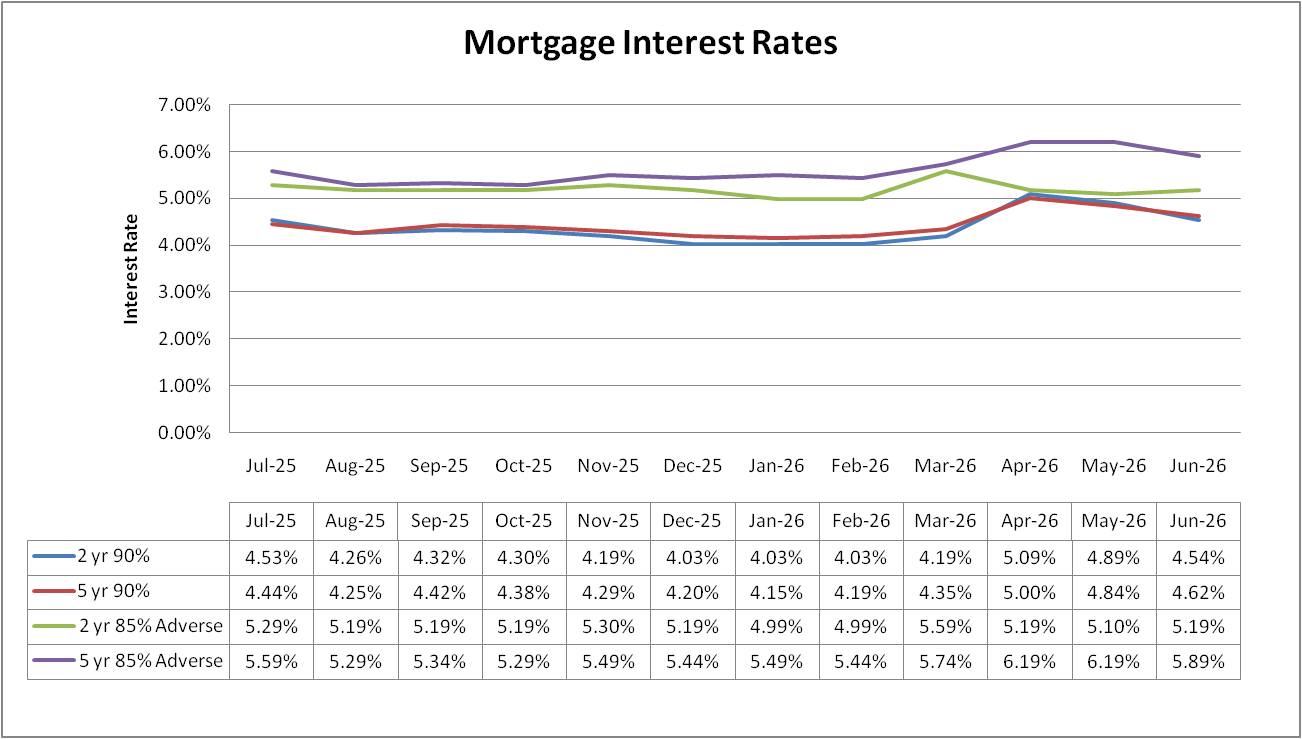

What mortgage rates we are looking at?

As ever, we always look at the same 4 scenarios for some consistency. The 4 scenarios are:

- 2 year deal at 90% LTV with a £999(ish) fee.

- 5 year deal at 90% LTV with a £999(ish) fee.

- 2 year deal at 85% LTV with a £999(ish) fee for adverse*

- 5 year deal at 85% LTV with a £999(ish) fee for adverse*

*Adverse in these examples is someone with 5 defaults from 2 years ago. Enough to mean we cant go to the high street.

With the adverse products, we were able to source 1,292 products.

Some of these lenders would not have actually accepted the adverse, some only lend in certain areas and some have large fees. When we put the rates below, we go with the ones we know are likely to accept the majority of people. That means there may actually be lower rates available on the market.

What mortgage rates are available now?

Generally speaking rates are on a downward trend.

The drops however are bigger than I was expecting to see which is great news for those looking for a mortgage. We are more or less back to where we were 10-12 months ago.

Hopefully this will continue to be the case.

Mortgage rates in 2026

There is a lot to consider…

- Andy Burnham for PM?

- Will this ceasefire hold?

- What will it look like after the ceasefire?

- Unemployment is a difficult conversation.

That is off the top of my head. There are things which should help inflation in the longer term. There are things that will also likely be a reason not to raise interest rates despite the inflation.

I am as they say “cautiously optimistic” that rates will continue to come down.

Summary – wait and see…

As I mentioned last month we seem to be doing a lot of variable rate products with no ERCs. One of the benefits of having a broker and talking through the options, most people instantly dismiss these but as soon as you talk about them people become open to them.

For people looking to move home but are unsure, the variable rate products offer a lot of flexibility without sitting on the SVR rate.

I think that seems to be the market we are in at the moment, “wait and see”.

On the upside, Canada are through to the last 16 (my daughter got them in the school sweepstake) and England are through to the last 32. Hopefully you have seen our flag in the village – we seem to be the only ones!